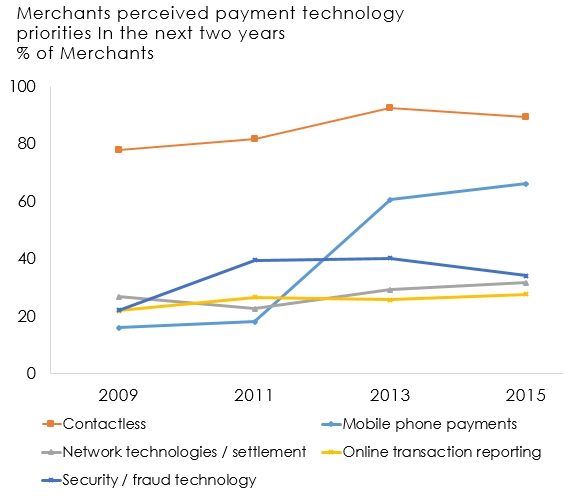

The Australian payments market is evolving rapidly in response to changing consumer behaviour, new technology acceptance and expanding popularity of debit card facilities. East & Partners has monitored these changing merchant payments and customer dynamics since launching the Merchant Acquiring and Cards Markets research program in 2004.

The program is based on direct interviews with a large scale natural sample of over 2,200 Australian merchants, both high street and online. The resulting analysis captures the collective “voice” of the merchant community, providing over a decade of valuable trending data and analysis coverage including transaction fees and surcharging behaviour analysis, future product and technology focus, online payments behaviour, receivables streams analysis, payment product acceptance and payment market statistics reanalysis.

More than a third of all merchants accept payments online, with a further 39 percent planning to do so. The momentum of online payments growth is unstoppable and on track to become one of the most dominant methods of payment in the market.

The Reserve Bank of Australia (RBA), following consideration by the Payments System Board, commenced a review of the regulatory framework for card payments in March 2015. The review follows recommendations from the Financial System Inquiry (FSI) that the Payments System Board consider a range of measures related to card payments regulation, particularly in relation to interchange fees and surcharging.

Reviewing payments regulation involves complex issues and potential reforms will require an extended period of time for consultation and implementation, with formal decision making on changes to interchange standards not expected before May 2016. The impact of these regulatory changes will be reflected in East & Partners Merchant Payments analysis. Currently a greater number of merchants are surcharging, but they are generally surcharging less.

Regulatory intervention in the payments market has already increased competition significantly. Subsequent reviews by the RBA and the focus on promoting transparency, consumer choice and innovation is gradually introducing a greater degree of efficiency and transparency into payments by allowing the forces of competition to establish a new market discipline.

For example, requiring merchants to limit their surcharging to a “reasonable cost of acceptance” continues to have an impact on surcharging activity.

| Distribution by Enterprise Segment | % of Total |

| Micro Business | 42 |

| SME | 30 |

| Lower Corporate | 14 |

| Institutional | 14 |

Subscribe

Subscribe